ITR Filing Deadlines for FY 2025-26: What Happens If You Miss the July 31 Date?

Every July, the Same Question Returns

As the income tax filing season approaches, many taxpayers find themselves asking the same question:

"Can I file my Income Tax Return later?"

Between collecting Form 16, reconciling investment proofs, reviewing bank statements, and balancing work commitments, filing an Income Tax Return (ITR) often moves to the bottom of the priority list.

Unfortunately, delaying your return can have financial consequences that extend well beyond a simple late filing fee.

Missing the due date may result in penalties, interest, delayed refunds, loss of tax benefits, and additional compliance obligations.

Whether you are a salaried employee, freelancer, business owner, investor, or NRI, understanding the filing deadlines for FY 2025-26 (Assessment Year 2026-27) is essential.

This guide explains the important dates, penalties, available options after missing the deadline, and practical steps you should take to remain compliant.

Understanding FY 2025-26 and AY 2026-27

Income earned between 1 April 2025 and 31 March 2026 belongs to Financial Year (FY) 2025-26.

The Income Tax Return for this income is filed during Assessment Year (AY) 2026-27.

Understanding this distinction helps taxpayers avoid filing errors and confusion while selecting the correct assessment year on the Income Tax portal.

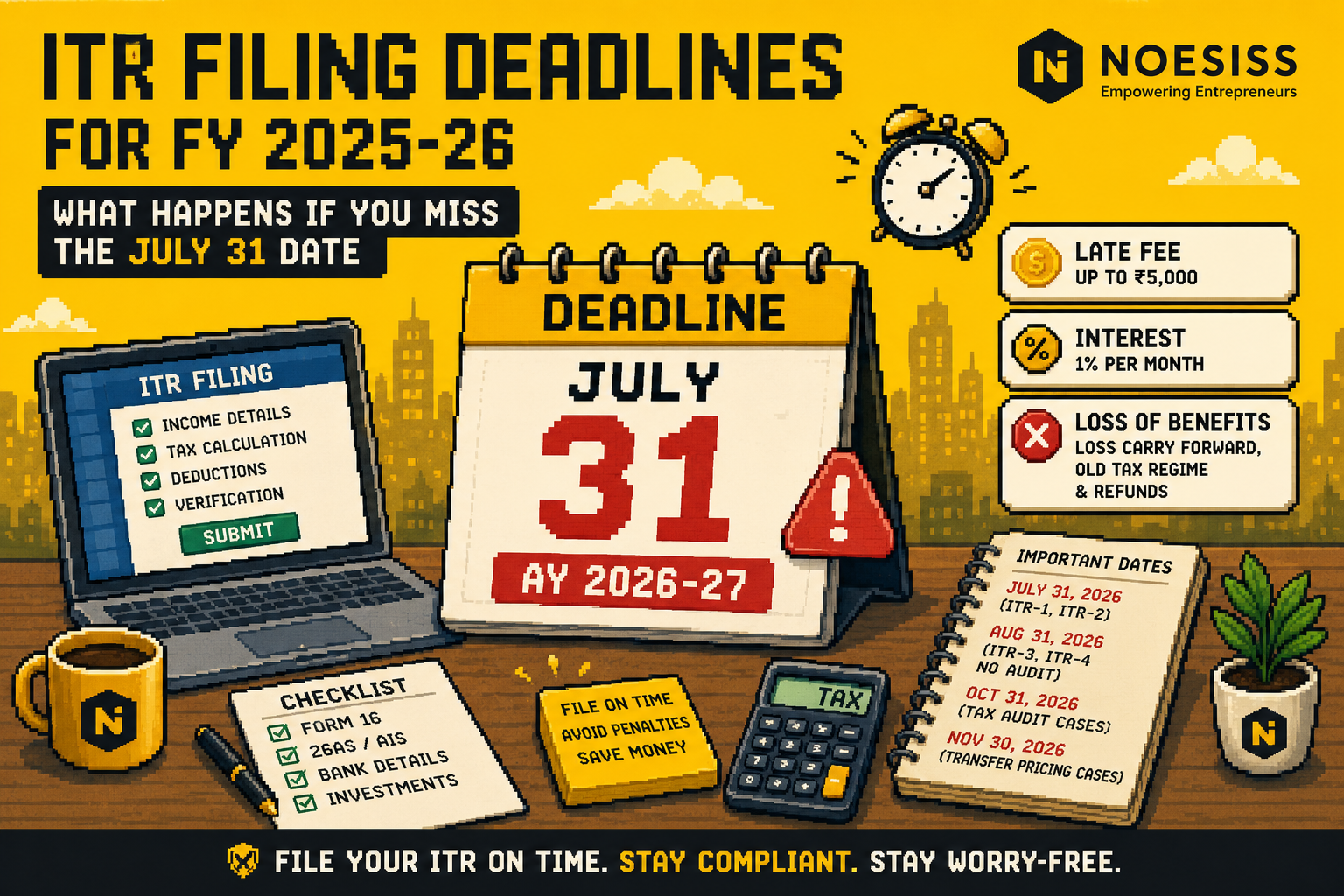

Important ITR Filing Deadlines

Different categories of taxpayers have different due dates.

Individual Taxpayers

The due date for most salaried employees, pensioners, and individuals filing ITR-1 or ITR-2 is:

31 July 2026

Professionals and Small Businesses

Individuals filing ITR-3 or ITR-4, where tax audit is not applicable, generally have until:

31 August 2026

Businesses Requiring Tax Audit

Businesses whose accounts require audit under the Income Tax Act generally have a due date of:

31 October 2026

Transfer Pricing Cases

Businesses involved in international or specified domestic transactions requiring a transfer pricing report generally have a due date of:

30 November 2026

As of now, no extension has been announced for AY 2026-27. Although deadlines have been extended in previous years due to technical issues or administrative reasons, taxpayers should avoid relying on possible extensions.

Filing early remains the safest approach.

What Happens If You Miss the July 31 Deadline?

Missing the due date affects more than just compliance.

Several financial and procedural consequences may apply.

Late Filing Fee Under Section 234F

Taxpayers whose total income exceeds ₹5 lakh may have to pay a late filing fee of:

₹5,000

If the total income is between the basic exemption limit and ₹5 lakh, the maximum late fee is:

₹1,000

Even taxpayers eligible for a refund may still be required to pay the applicable late filing fee.

Interest Under Section 234A

Where tax remains unpaid beyond the due date, interest under Section 234A is charged at:

1% per month or part thereof

The interest continues until the outstanding tax liability is paid.

Delaying your return therefore increases the total amount payable every month.

Loss of Carry Forward Benefits

One of the most overlooked consequences of late filing is the inability to carry forward certain losses.

This may affect:

Capital losses

Business losses

For investors and business owners, losing this benefit could increase tax liability in future years.

Impact on Tax Regime Selection

For eligible taxpayers with business income, filing after the prescribed due date may restrict certain tax regime choices.

This can affect taxpayers claiming deductions such as:

Section 80C

Home loan interest

House Rent Allowance (HRA)

Other eligible deductions

Choosing the correct tax regime before filing is therefore important.

Delayed Income Tax Refunds

Many taxpayers file returns primarily to receive refunds.

Late filing generally delays refund processing because returns submitted after the due date are processed later.

For taxpayers expecting substantial refunds, filing early improves the likelihood of receiving money sooner.

Filing a Belated Return

Missing the original deadline does not mean you lose the opportunity to file your return.

You may still submit a Belated Return under Section 139(4), subject to applicable legal timelines.

However, filing late generally results in:

Late filing fee

Interest on unpaid tax

Delay in refund processing

Possible loss of certain tax benefits

Even with these consequences, filing a belated return is significantly better than not filing at all.

Revised Return

If you file your return on time and later discover an error, the Income Tax Act allows you to submit a revised return.

A revised return can correct:

Incorrect income reporting

Missed deductions

Wrong bank account details

Capital gains errors

Other reporting mistakes

Filing a revised return ensures your tax records remain accurate and reduces future compliance issues.

The Updated Return (ITR-U): A Final Opportunity

If you discover omitted income after the standard filing deadlines have passed, the Updated Return (ITR-U) provides one final opportunity to voluntarily correct your tax records.

An ITR-U can generally be filed for up to four years from the end of the relevant Assessment Year, subject to the applicable provisions of the Income Tax Act.

However, this facility comes with an additional tax liability.

Depending on when the updated return is filed, taxpayers may be required to pay:

Additional tax of 25% of the tax and interest due (within the prescribed period).

Additional tax of 50% if filed in the later prescribed period.

An Updated Return cannot be used to:

Claim a refund.

Reduce an already assessed tax liability.

Declare a loss that was not previously reported.

Its purpose is to voluntarily disclose omitted income before enforcement action is initiated by the tax authorities.

The New Income Tax Act 2025

The Income Tax Act, 2025 introduces several structural changes, including replacing the concepts of Previous Year and Assessment Year with a single Tax Year.

However, for FY 2025-26 (AY 2026-27), taxpayers will continue filing their returns under the provisions of the Income Tax Act, 1961.

This means:

Existing ITR forms remain applicable.

Existing due dates continue to apply.

Existing compliance requirements remain unchanged.

There is no need to learn an entirely new filing framework for the current filing season.

Practical Checklist Before Filing Your ITR

Preparing in advance helps avoid mistakes and last-minute stress.

Before filing your return, ensure you have:

Form 16 from your employer.

Form 26AS.

Annual Information Statement (AIS).

PAN and Aadhaar details.

Bank account information.

Interest certificates from banks.

Capital gains statements from brokers or mutual funds.

Investment proofs.

Home loan interest certificate (if applicable).

Rental income details (if applicable).

Business or professional income records (if applicable).

Review every document carefully before submission.

Small mismatches often lead to notices or delays in processing.

Best Practices for Timely ITR Filing

A few simple habits can make tax filing significantly easier every year.

File Early

Avoid waiting until the last week of July.

The Income Tax portal experiences heavy traffic close to the deadline, increasing the likelihood of technical issues.

Verify Your Return

Filing alone is not enough.

Complete e-verification within the prescribed timeline to ensure your return is treated as valid.

Compare Tax Regimes

Before submitting your return, compare both the Old Tax Regime and the New Tax Regime.

Choosing the right regime can reduce your tax liability considerably.

Reconcile AIS and Form 26AS

Always compare your return with:

Annual Information Statement (AIS)

Form 26AS

This helps identify missing income, TDS mismatches, or reporting errors before filing.

Keep Supporting Documents

Maintain copies of:

Salary documents.

Investment proofs.

Tax payment challans.

Capital gains reports.

Rental agreements.

Loan certificates.

These documents may be required during assessments or future verification.

Why Professional Assistance Matters

Income tax filing today is far more than simply filling out an online form.

A professional review helps identify:

Missed deductions.

Incorrect TDS entries.

Capital gains computation errors.

Incorrect tax regime selection.

AIS mismatches.

Reporting omissions.

Professional guidance also reduces the risk of notices, penalties, and unnecessary tax outflows.

How Noesiss Can Help

At Noesiss, we simplify income tax compliance for salaried professionals, entrepreneurs, freelancers, startups, and NRIs.

Our services include:

Income Tax Return (ITR) filing.

AIS and Form 26AS reconciliation.

Tax regime comparison.

Capital gains computation.

Income tax advisory.

Notice response assistance.

Tax planning and compliance.

Our objective is not just to help you file an Income Tax Return but to ensure it is accurate, compliant, and optimized for your financial situation.

Final Thoughts

Filing your Income Tax Return on time is more than a statutory obligation.

It protects your financial interests, preserves important tax benefits, improves compliance, and reduces unnecessary penalties.

Whether you are expecting a refund, carrying forward losses, claiming deductions, or simply remaining compliant, timely filing gives you greater financial certainty and peace of mind.

Rather than waiting until the deadline approaches, prepare your documents early, verify your information carefully, and complete your filing well in advance.

At Noesiss, we help individuals and businesses navigate the filing process with confidence by providing accurate, timely, and practical tax compliance support.

A timely Income Tax Return today can save significant time, money, and stress tomorrow.